What is a Credit Score?

- 28 March 2017 | 3698 Views | By Mint2Save

Your credit score may result the difference between being deprived of, or approved for credit, and a low or high interest rate. A good score can benefit you for qualifying for an apartment payment and even help you get utilities connected, when short of a deposit.

What is it?

Your credit score is a 3-digit number produced by a mathematical algorithm using information in your credit report. It is made to predict risk, specifically, the possibility that you will become seriously aberrant on your credit obligations in the 24 months after scoring. In other words, it is a tool used by lenders to determine whether you qualify for a particular credit card, loan, mortgage or service. Through the information on your credit report and any other additional information you supplied as part of your application, lenders use a mathematical model to calculate a score that signifies your credit history. This helps to specify what kind of borrower you are, and how probable it is that you will manage your repayments.

During all your life, your credit score will play a key role in the monetary products you take out. For instance, when you apply for a credit card, it will determine whether your application is accepted and what interest rate you pay. People having a higher score are mostly seen as lower risk, meaning the lenders are more probable to give them credit. It should be noted that each lender follows a different policy for credit scoring. Therefore, if you don’t qualify the criteria of one lender, you may still be able to get credit from another based upon the same score. It all depends on the lender’s criteria.

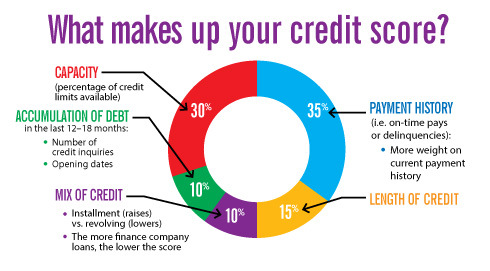

Factors affecting credit score:

The credit score is based on the credit report. Numerous different factors on your credit report can result in your credit score to change, including:

- Data on your credit report such as how much of your available credit you’re using and your entire debts

- The history of credit account payments.

- Credit searches (when a credit application is designed)

- Public records (electoral roll and county court judgments (CCJs))

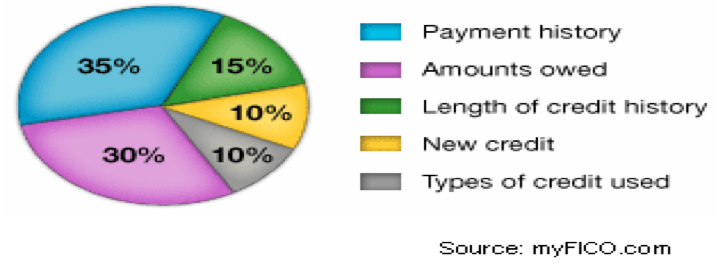

FICO:

There are a mass of credit-scoring models in existence, but the one that dominates the market: the FICO credit score.

In accordance with myFICO.com, which is the customer website for the FICO score developer – 90% of all financial institutions in the U.S., use FICO scores in their decision making process.

There are three FICO scores, one for every credit report provided by the three major credit bureaus: Equifax, Experian and TransUnion. Consumers currently can get access to only Equifax and TransUnion FICO scores. Experian terminated its agreement with myFICO.com in 2009.

Following pie chart shows the Elements of your Credit score:

An idea about a Good Credit Score?

It depends on lenders, so each lender decides how to use these numbers. Anyways, here are some basic guidelines:

760 – 850: Excellent

720 – 760: Very good

680 – 720: Average – very good

620 – 680: Fair – poor

Below 620: Poor

Check your credit score:

Federal law instructions the consumer’s right to a free credit report each year from each credit reporting agency, but not to a free credit score. You can use the FICO score estimator to know your score range free of charge. To get the exact number, you have to buy it from a score provider, for instance, myFICO.com or any of the reporting agencies.

IMPORTANT THINGS TO NOTE ABOUT CREDIT SCORE:

Credit Score

- Scores Are Based on 5 Essential Factors:

The factors being payment history, credit utilization, average credit age, account mix and inquiries.

- Credit Can Help You find Fraud

In case someone runs up a large credit card bill or takes out credit in your name, it will show up on your credit report and alter your credit score. So you can watch your score for changes you did not expect.

- Negative Information Ultimately Ages Off

Various types of negative information will be there on your credit report for different periods of time (bankruptcy is an exception), but usually, negative information ages of and does not affect your score after 7 years.

- The major factors involved in the calculation of a credit score are the number of accounts you have and the types.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18337 Views

- 16 June 2020 | 15813 Views

- 19 May 2021 | 15352 Views

- 14 May 2021 | 12080 Views

Recent