Latest Rule for Income Tax Filing in India

- 13 May 2017 | 4156 Views | By Mint2Save

Everybody is aware of Income Tax; it is a central part of the revenue generation system of the Indian government. Amongst the huge number of taxes present in the system in India, income tax is the one which deals with the taxation of the monthly earnings, though it is calculated on an annual basis of every individual, business and corporate and other establishment in a financial year. Earnings or the income may be in the form of regular wages, interest, capital gains, dividends or any other profits.

New Income Tax Changes from April 2017 by Income Tax Department

In the Budget of 2017, there are several changes related to income tax were announced. These changes have occurred since April 1, 2017. Some of the important changes are as follows:

- The income tax rate for people earning Rs.2.5 lakh to Rs.5 lakh per year has now reduced from10% to 5%, because of which individual saves tax of up to Rs 12,500 per year and Rs 14,806 for people whose income is above Rs 1 crore.

- For those people who are earning the income of Rs 50 lakh to Rs 1 crore, a surcharge of 10 per cent of the tax rates will be charged. And for the people earning above Rs 1 crore then the surcharge rate is untouched at 15 per cent.

- For the people earning up to Rs.5 lakhs filing of ITR become easy for them as the government has introduced a single page 1 page form for them. Those people who file their ITR through this form will not be examined by the Income Tax Department.

- From the assessment year 2018-2019, no deductions can be claimed for the investments that are made under the Rajiv Gandhi Equity Saving Scheme.

- If the people do not file Income Tax returns for the current financial year (2017-2018) on time, then they will have to pay a penalty of Rs. 5,000 till December 2017 and if filed after December 2017 they will have to pay Rs. 10,000. For the people whose earnings are up to Rs. 5 lakh, then they have to pay the penalty of Rs 1,000.

- According to the Economic Times Report, the time period for holding long-term immovable property now has been reduced from 3 years to 2 years. The long term immovable property if hold beyond 2 years, then it will be taxed at a rate of 20% and person will be entitled to many exemptions on reinvestment.

- Under the long term capital gain Tax, the base year to adjust prices for inflation has been changed from April 1, 1981 to April 1, 2001 and hence it will result in lower profits on sale. If people reinvest in some redeemable bonds, then only tax exemption will be available for them.

- In addition, tax exemption will be available on the reinvestment of long term capital gains which is available for investments in REC and NHAI bonds only.

- From June 2017 onwards, 5% TDS will be subtracted for the people whose rental payments are more than Rs. 50,000 per month.

- And also from July 1, 2017, without having Adhaar, people will not be able to file their ITR.

- Previously the time period of revision of Income Tax was 2 years and now it has been reduced to 1-year applicable from the end of the current financial year, or prior the completion of assessment year, whichever is former.

- Those people who are making partial withdrawals from National Pension System are not required to pay tax on the same. They are allowed to take withdrawal 25% before retiring in the case of emergencies.

- Moreover, Health insurance, Car insurance, Two-wheeler insurance premiums get increased from April 1, 2017.

Following are the Current Income Tax slab rates for the Financial Year 2017-2018

For Individual Payers and HUF (Age less than 60 years):

| Income Slab | Tax Rate |

| Income up to Rs. 2,50,000* | No Tax |

| Income from Rs. 2,50,000 – Rs. 5,00,000 | 5% |

| Income from Rs. 5,00,000 – 10,00,000 | 20% |

| Income more than Rs. 10,00,000 | 30% |

For Individual payers and HUF (Age more than 60 years but less than 80 years):

| Income Slab | Tax Rate |

| Income up to Rs. 3,00,000* | No Tax |

| Income from Rs. 3,00,000 – Rs. 5,00,000 | 5% |

| Income from Rs. 5,00,000 – 10,00,000 | 20% |

| Income more than Rs. 10,00,000 | 30% |

For the Super Senior citizens (Age more than 80 years):

| Income Slab | Tax Rate |

| Income up to Rs. 2,50,000* | No Tax |

| Income up to Rs. 5,00,000* | No Tax |

| Income from Rs. 5,00,000 – 10,00,000 | 20% |

| Income more than Rs. 10,00,000 | 30% |

Other than above-related changes made by the Indian government, there are many other changes that are introduced. So, the people must stay updated about these changes as every individual has a direct impact on their income tax.

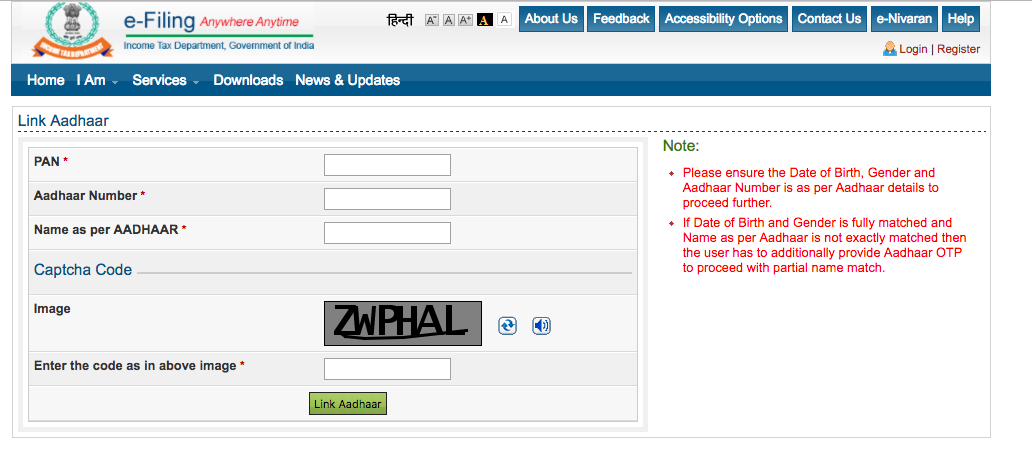

Linking Aadhar Card with Income Tax Department

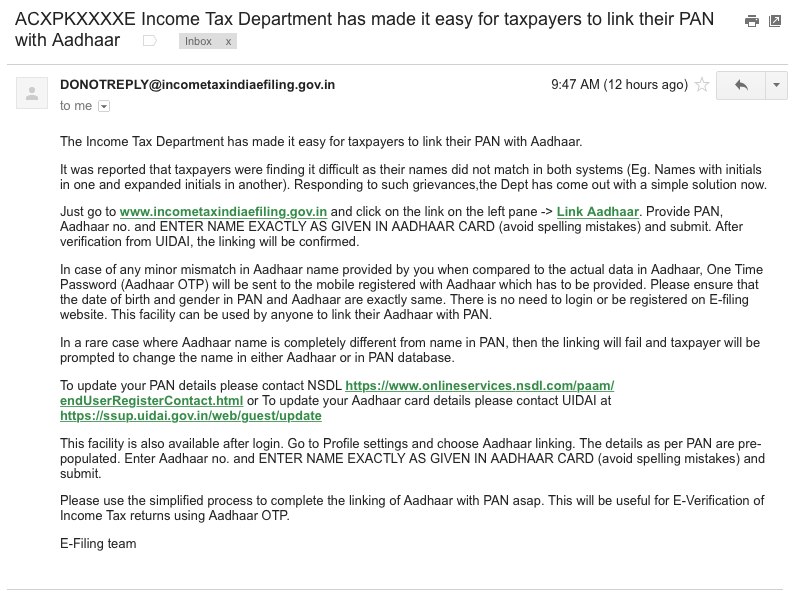

Adding a latest feature with income tax returns is the compulsion to link UIDAI’s Aadhar Card with your PAN Card. The linking has been mandatory for filing income tax returns.

In order to provide information and convenience to customers regarding the same, the Income Tax Department has been sending emails and messages to those who already have provided communication data to them.

This compulsion has been introduced in the Finance Act, 2017. When subsidies were linked with Aadhar Number, it became quite obvious and necessary to link these two.

Since the flow of subsidies has been flawed and faced severe criticism for uneven distribution, linking would reduce the outflow of unnecessary subsidies that people get into their account.

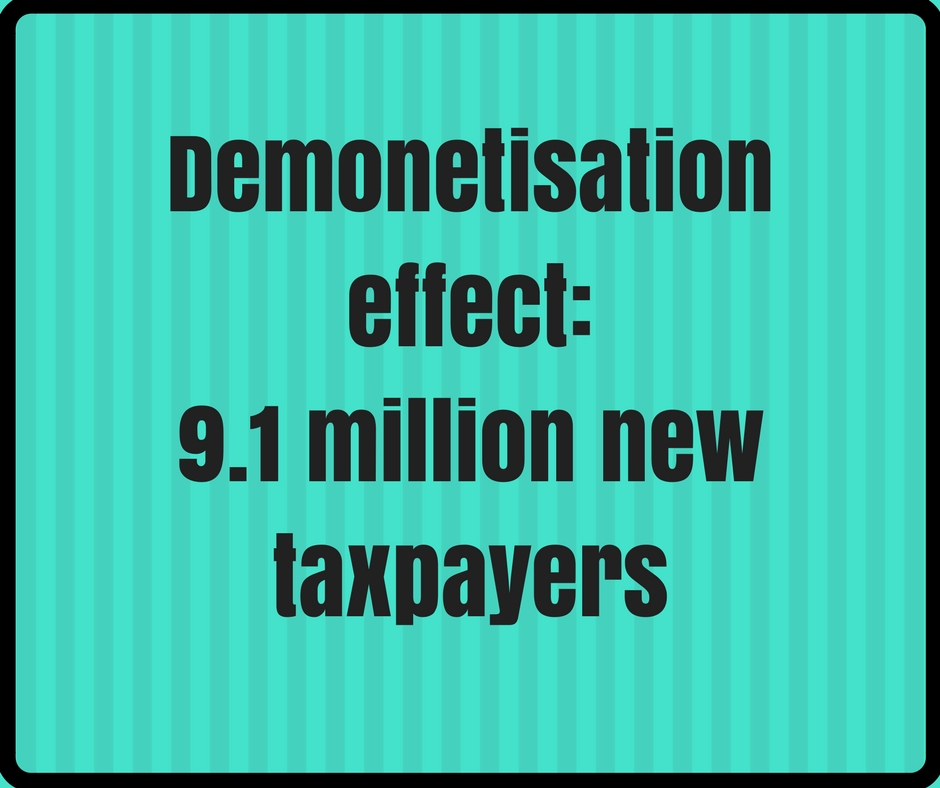

Post demonetization, the number of people filing income tax has increased dramatically during this fiscal year.

However, filing of income tax returns, doesn’t guarantee increased revenue as there may not be any tax liability. When considered holistically as a strategy, income tax filing would be streamlined, which would further reflect when real estate purchase deals would be linked via Aadhar Card.

The intention of the government is quite clear with these alphanumeric numbers. The whole system ranging from one’s assets to liabilities is going to be recorded and monitored all the time. Linking Aadhar would further confirm your financial status in a more transparent manner.

As the officials unearth more and more information about the status of black money, income tax rules are bound to change. This could also mean imposition of more wealth related taxes.

However, as of now, this seems a long journey as tax filing for last year is yet to reach the massive momentum.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18203 Views

- 16 June 2020 | 15735 Views

- 19 May 2021 | 15296 Views

- 14 May 2021 | 12012 Views

Recent