Investment v/s Inflation

- 25 March 2017 | 1409 Views | By Mint2Save

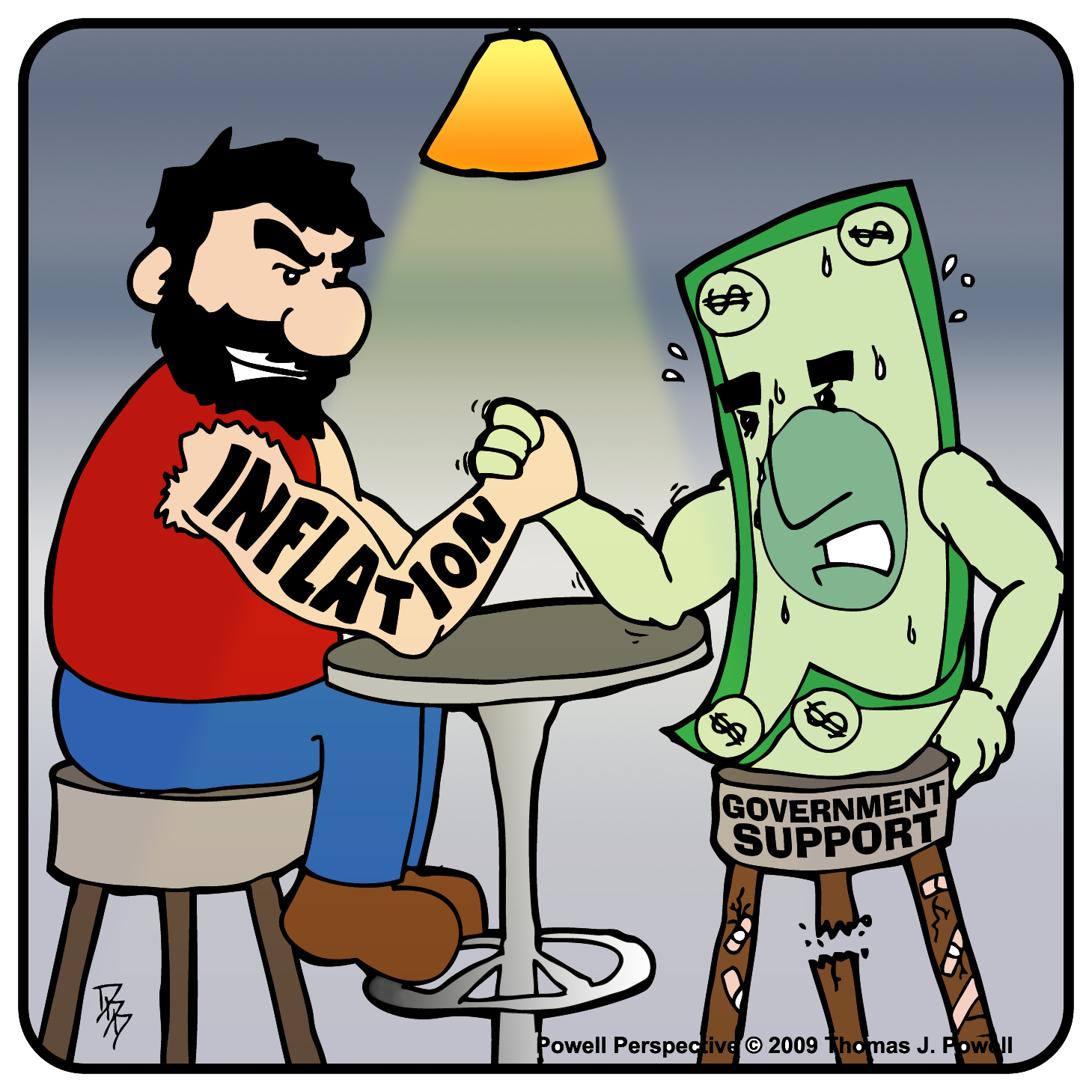

A widely debated concept, Inflation is an economy-wide continuous tendency of increasing prices from one year to the next year. The rate of inflation is very important to understand as the real value of any investment gets eroded due to the inflation rate and the loss in spending power over time. To maintain Standard of living, inflation also tells investors exactly how much of a return (%) on their investments need to make for them.

Suppose you can buy a burger for $3 this year and the inflation this year is 10%. Theoretically, 10% inflation means that next year the same burger will cost you 10% more i.e. $3.30. So, at least at the same rate of inflation if your income doesn’t increase, you will not be able to buy more burgers. Though, inflation is eventually about growth of money, and it is an indication of too much money chasing too small number of products.

For the people who are living on a fixed income, inflation is a very significant subject for them, such as retirees. Investors should purchase investment products with returns that are higher or equal to the inflation rate. For example, if XYZ stock returned 3% and inflation was 4%, then the real return on investment would be minus 1% (4%-3%).

The effect of inflation on your portfolio depends on the type of securities you hold. Stocks generally give a good reflection on inflation hedges over the long run as companies are able to charge higher prices to offset rising cost. Especially over shorter horizons, stock returns, may lag inflation. Match your goals and risk acceptance with an appropriate mix of investment. The major problem with inflation and stocks is that a company’s return tends to be overstated. Stock market investors do not just want prices to rise; in fact, they need the stock price to increase more than the rate of inflation to make real money. If not, then they effectively lose money. When a company looks like it’s prospering, the reason behind the growth is inflation, especially in times of high inflation.

One Best way of staying in front of inflation is buying stocks that pay you good dividends. The rate of interest offered by banks is usually much less than the inflation rate. Dividends can be calculated annually, just like inflation.

This method is called the dividend yield which can be measured by adding dividends received during the year and dividing it by the stock price. The dividend yield must be higher than the annual inflation rate. Gold is considered an ideal evade against inflation. As per a market expert if one can afford to spend a bigger sum, then real estate can also be an option.

Bond prices will drop if either there is a rise in inflation rate or interest rate. When interest rates rise, bond prices fall, thus, inflation may lead to a fall in bond prices, potentially reducing total returns on bonds. Most investors aim to increase their long-term purchasing power. Inflation puts this goal at risk because returns on investment must first keep up with the rate of inflation in order to increase real purchasing power. Inflation can be harmful to fixed income returns, If investors do not protect their portfolios. Many investors purchase fixed income securities because they want a stable income stream, which comes in the form of payments, interest, or coupon. However, because the rate of interest, or coupon, as inflation rises, most fixed income securities remain the same until maturity, the purchasing power of the interest payments declines.

The effect of inflation on investment occurs directly and indirectly. Inflation increases transactional and information costs, which directly hinder economic development.

Individual investors have the greatest need for inflation hedges, because they save for retirement. Those investors are not looking for absolute funds when they retire; they are looking for purchasing power. They cannot consume dollars, but however they will need to consume groceries, health care, gasoline and a host of other living expense and those expenses will definitely go up with the rise in inflation. The individual is not like a foundation that can cut back on its funding of grants. Those individual investors are responsible for investments, have a greater exposure to inflation and hence the greatest need for real return assets.

If safety isn’t your top priority, be mindful of the impact of inflation. At last, Inflation will always be a silent thief that will eat the value of your investments, but with some awareness and good planning, you will be able to deal with the same and maintain the purchasing power of your savings.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 15289 Views

- 16 June 2020 | 12777 Views

- 19 May 2021 | 12300 Views

- 14 May 2021 | 8107 Views

Recent

- 22 December 2023

- 17 December 2023

- 16 December 2023