How Does Depreciation Work?

- 14 April 2017 | 1323 Views | By Mint2Save

When it comes to fixed assets, such as machinery, furniture, etc., every business entity not only wants to accumulate the best, but also seeks to take the maximum benefit from them. Apart from meeting the usual demand of production and supply, these fixed assets also give a much necessary benefit of depreciation.

Depreciation is the process which allows the small business owners to reduce or decrease the value of an asset over time, due to its age, decay and wear and tear.

It is a deduction in income tax that allows you to recover the cost of assets like, furniture, cars and other equipments that you purchase and use in your business.

Generally, any of the fixed assets that may be a long term asset cannot be easily converted to cash can be depreciated. This also includes intangible property such as patents and software. When you spend, say, $50,000 on an asset, you wouldn’t necessarily claim a $60,000 expense upfront; rather, you’d depreciate the asset over time, eventually claiming the full cost.

There are many ways that you can use depreciation as a tax deduction and as an expense that you generally record in the books of accounting. Taxes are what most people think of when they hear the word depreciation. You use depreciation to decrease your tax burden, as you are lowering your overall taxable income. But it is very important to understand that depreciation is a non-cash expense, though it does not affect your company’s cash flow or its actual cash balance.

For example, let’s say you own a restaurant that earns $200,000 in net income in a year the money you have earned after accounting for all costs of operating your business which includes operating expenses and investments but you take total depreciation deductions of $25,000 on the building you own. The IRS would tax you on $175,000 of income instead of $200,000 due to the deduction.

A taxpayer is allowed to depreciate the property if it meets some requirement such as: property must be owned by the person who pays taxes; a taxpayer must use the rental property in business or in an income-producing activity. If a taxpayer uses a property for personal purposes or business, the taxpayer gets a depreciation deduction based only on the business use of that property.

The property must last more than one year. Depreciation begins, for example: Suppose you buy a rental property on June 15. After several months, you have the property ready to rent on August15, so you start to advertise online and in the local newspapers. You find a tenant, and his rent begins on October 1. Since the house was placed in service (that is, ready to be occupied) on August 15, you would begin to depreciate the house or to collect the rent form the tenant in August (not in October).

You must keep the records to calculate the depreciation which should involve a copy of the invoice that shows what you bought and also the proof of payment. To make sure you paid the applicable sales tax on the asset, many states will check assets you purchase. Even if you purchased the asset in another state, you must pay use tax to your state if sales tax was not charged.

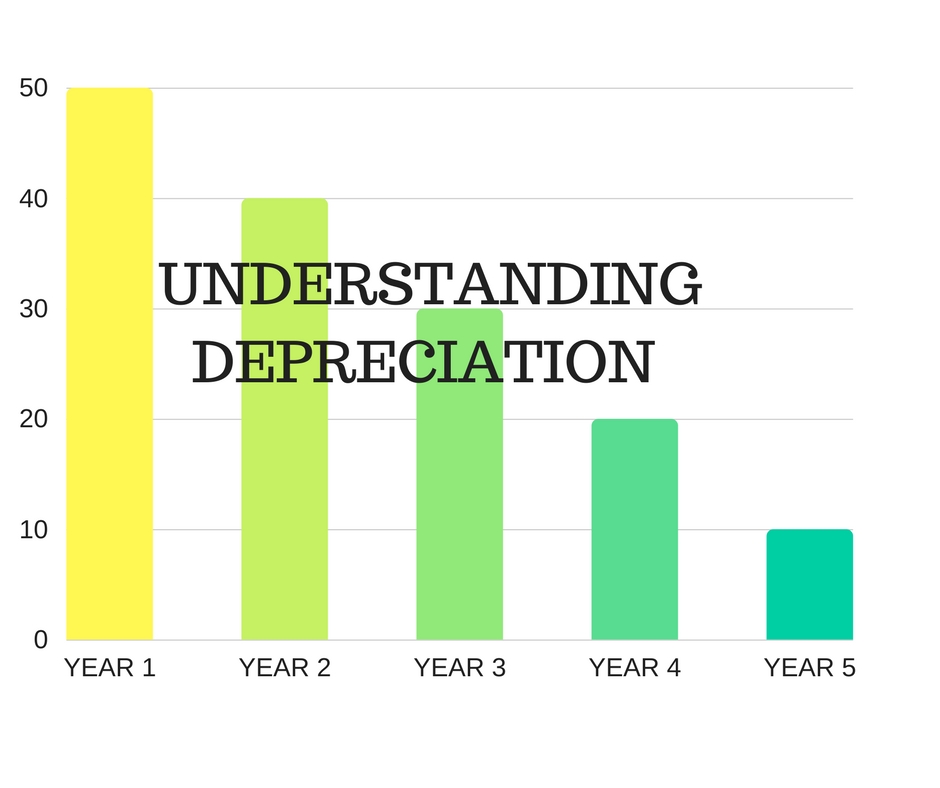

There are three ways of calculating depreciation. The first is straight line method, simply assumes an equal amount of depreciation each year of the asset’s life. The next two which may sound off putting, but which are delightfully simple, are known as units of production depreciation and double-declining balance depreciation.

Unit-of-production depreciation is a two-step process, used to calculate depreciation for assets whose valuable life is measured in output capability rather than years. If you want to depreciate an asset based on its actual usage level, then the units of production method are suitable but, it is commonly used with airplane engines that have specific life spans fixed to their usage levels.

There are three factors that are considered when you calculate depreciation which are: Useful life, depreciation is known over the useful life of an asset. Salvage value- When a company in due course disposes of an asset, it may be able to sell it for any reduced amount, which is the salvage value and the Depreciation method, where you can calculate depreciation expense using an accelerated depreciation method which help you to recognize more depreciation early in the life of a fixed asset.

Smoothing your income is not just about making your finances appear reliable. Depreciating of an asset also gives you a right path of how much it actually costs to run your business and sell products. You won’t see that expense listed in following months once, if your expense, operating assets right away that equipment starts to support or produce revenue. By spreading out the expense of asset purchases, depreciating them gives you a better sense of your true monthly profit.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 15289 Views

- 16 June 2020 | 12777 Views

- 19 May 2021 | 12300 Views

- 14 May 2021 | 8108 Views

Recent

- 22 December 2023

- 17 December 2023

- 16 December 2023