Home Mortgage Insurance

- 4 April 2017 | 3584 Views | By Mint2Save

Getting a mortgage based loan is not an easy task, neither for the lender, nor for the debtor. It requires a thorough process of risk assessment, legal, valuation, and several other necessary formalities. One of the most common mortgage based loan sought all over the world is none other than the home loan. These loans, one’s getaway to establish a safe place to reside where families can prosper, are often a two way victory. The lender earns interest, various non commission based income and goodwill, while the debtor gets a very tangible piece of property.

There is no doubt that such loans often involve a high sum of money involved and be whatever the case, nobody wants to risk the money involved, neither the bank, nor the borrower. So, as a very gullible solution to address mortgage loans when they are unpaid is to take the shelter of private mortgage insurance, or pmi.

Private mortgage insurance becomes an utter necessary when we try to purchase an expensive property by merely paying 10 or 20 percent as its down payment. Knowing how risky the business can be, banks usually apply a primary mortgage insurance to every home loan. This insurance gives a fair protection to the bank against the money it has lent. Further, the customer can also get rid of most of financial issues that may arise when there is no earner left to service the installments of the loan.

With the increasing purchasing power of the retail consumer, mortgage insurance has received prime importance and much deserved attention. This too, has been for obvious reasons, out of which, the main reason is to not to let the real estate property become a burden for anyone.

Since this insurance is done customer wise for every mortgage backed loan, it is also called private mortgage insurance (PMI).

The benefits of having a Private Mortgage Insurance

- Single Plan: A single life cover can cover each of the borrower on a joint loan. It saves a load of paperwork, money and, obviously time.

- Loan Protection: Insurance of your home mortgage loan helps to protect your family in your absence. In a situation of the unfortunate failure of the loan borrower then the insurance company settles the loan amount with the lender or bank. The surplus amount is given to the beneficiary of the policy holder.

- Tax benefits: While making an insurance of your home loan you get tax benefits under section 80C and 80D of Income Tax Act and thus depends upon how often you choose to pay premium either yearly, half-yearly or monthly.

- Health Protection: You get life plus health insurance such as critical illness or disability in one plan. You get paid on initial diagnosis of 34 critical illnesses.

- Premium: A Person who is eligible for a home loan is also eligible for home loan insurance. Your insurance premium that is broken down into little amounts is added to your EMI. While paying a small premium on the total sum insured, then you must keep in mind that you are also paying an interest on the premium amount too. So, higher the tenure, then higher will be the premium. In the same way, higher is the premium amount if higher the age. For an individual it is mandatory to have medical test at the age above 40 years.

- Loan tenure: The premium of your insurance will increase with the period of the loan. For instance, a cover of Rs 5 million for 6 years years and a cover of Rs 50 lakh for 20 years will draw different premiums with the last being more expensive.

- Saving & Control: If you reimburse your home loan early, you can continue with this plan to protect your loved ones against unfortunate events.

This home loan insurance plan covers only the outstanding loan liability from the time it is taken. In a situation when the applicant is not able to repay the loan, then the proceeds of the home loan insurance cover help the family to pay back the outstanding amount. In addition, home loan insurance allows people with limited savings to purchase homes prior by guaranteeing the full amount of the mortgage. Suppose your home loan is covered, then your lender will not be burdened with the extra risk that you may fail to pay in case of any misfortune. Other than that purchasing a home without any loan insurance have need of a larger down payment. So, it is always advisable to the individual to go for a home loan insurance policy.

Many times borrowers have two thoughts in mind that if they should go for a separate life insurance plan or should they buy one that is being provided by the bank along with the home loan. Experts believe that the home loan insurance is same as to any other life insurance term plan. The basic difference between them is that instead of paying your nominee the insurer resolves the claim with the bank to shut the loan on behalf of the policy holder. Here the full money will be given to your nominee or the legal beneficiary, who consecutively would then have to settle the loan with the bank. The borrower’s family can use if some money is left. On the other side of mortgage insurance, your sum guaranteed keeps reducing with the outstanding amount.

Experts note that home insurance covers are expensive than the general term plans. At the same moment, if you have taken a decision to transfer your home loan from one bank to another, then you may lose your premium that is paid on home loan insurance with the prior bank. Although it is a clever decision of buying home loan insurance from your bank.

Mortgage Insurance Premium

One critical aspect of mortgage insurance is the calculation of the premium. The premium depends on a lot of factors which as inter dependant on each other, such as:

- Age of the borrower

- Amount of loan to be taken.

- Credit Score of the borrower.

- Pricing which is set by the lending bank.

- Risk premium set by insurance.

- Market trends.

- Government Policies.

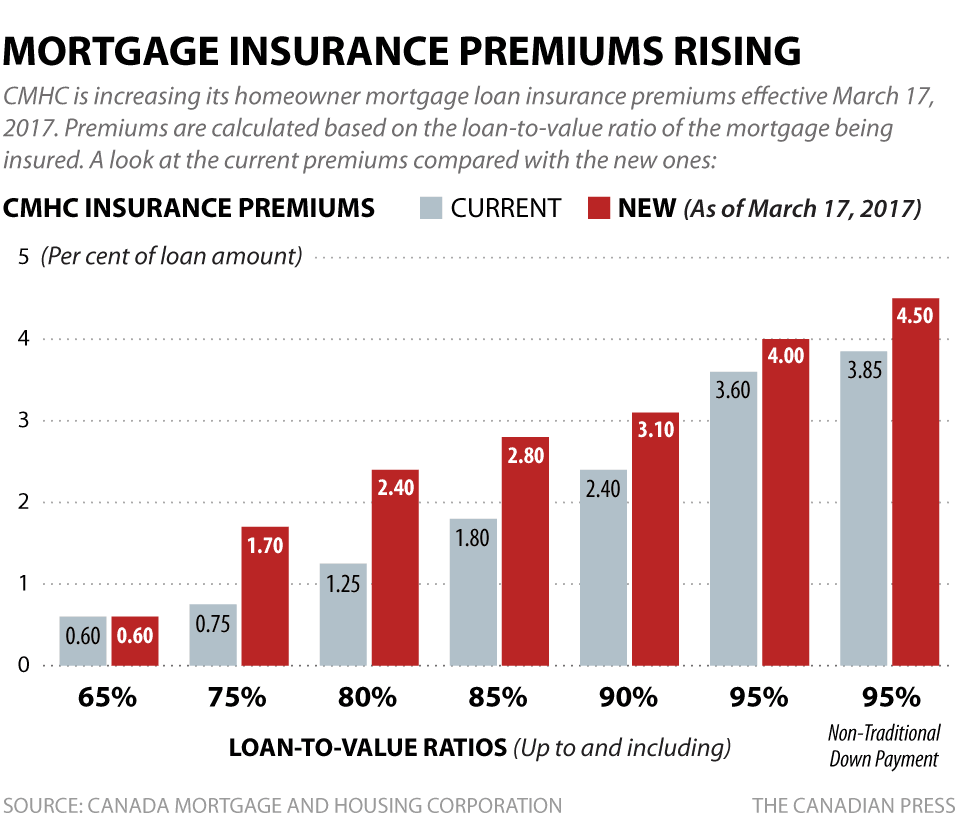

As obvious from these few critical points, mortgage insurance premium is unique for almost every mortgage backed loan. These premiums are on a rise as shown in this image:

Lending in the real estate sector is often considered as evergreen outstanding exposure. Why? Firstly, the supply and demand go hand in hand and there is always a price for a piece. Secondly, the government policies have been quite encouraging to let everyone have a home that they deserve. The last, but not the least, asset creation. The lender and the debtor, both will have an asset creation. The sheath that mortgage insurance provides makes sure that no one is left insecure.

So, “Never resist from buying a Private Mortgage Insurance, which will encourage the bank to grant loans as well as have confidence in you”

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18241 Views

- 16 June 2020 | 15762 Views

- 19 May 2021 | 15315 Views

- 14 May 2021 | 12036 Views

Recent